A TFI research project by Jay Zenkić, Kobe Millet, and Nicole Mead

Do you think you spend more when you have coins or banknotes in your wallet? In this report, we show that carrying coins instead of notes can cause you to spend, donate, and even gamble more.

Cash comes in two forms: coins and banknotes. Paper notes are convenient because they’re easy to fold up and carry, while coins are more durable, lasting longer. But people don’t seem to like coins: those heavy flat discs may actually be hindering them from saving more for their future. Using currencies with the same denomination in both coins and banknotes – cash in countries like India and Hong Kong – we show that people from Europe, the USA and India will part with more cash when burdened by coins instead of carrying equivalently valued banknotes. We argue that transferring coins to digital currency may be one short-term solution to this problem.

Cash is Still King

Most people believe that cash is on its way out, so why worry? From a global perspective, however, it’s important to stress that cash is still a vital form of payment. These days, there is more cash in circulation than ten years ago, when smartphones were still a rarity. People also still spend cash on a daily basis. In the Eurozone, 79% of all point-of-sale payments are made in cash and the most common form of payment in the USA is, indeed, still cash. The poorest people rely on cash the most, which shows that the physical characteristics of cash may be yet another obstacle for those struggling with poverty.

But do people spend coins and banknotes differently? Classic economic theory would say no: all forms of money should be spent to the same extent. However, behavioural researchers have found that cash is especially “painful” to spend when compared to other kinds of money, such as credit cards and cheques.

The Pain of Paying and Holding

Researchers argue that cash is particularly painful to spend because it’s the most tactile form of cash: to pay with cash, you have to take it out and count it, whereas paying with your credit card involves a simple swipe. Coins are looser, heavier, and more noticeable than banknotes – does this suggest that coins are more painful to part with than banknotes?

The physical aspects of coins are usually seen as negative: they’re bulky, heavy, cumbersome. In fact, Chinese merchants invented banknotes because of the cumbersome nature of coins. Their coins had holes in them so they could be strung together, but when these strings of coins became too heavy, the merchants would exchange the coins for paper notes.

Because coins are bulkier and heavier than banknotes, we expect that many people find them a nuisance to keep. We therefore hypothesized that, when given the opportunity, people would be more inclined to spend their coins rather than their notes.

Finding 1: The Spending of Coins

To test if people would spend more coins than equivalently valued notes, we studied shopping behaviour in a rural Indian setting in May 2019. We chose India for several reasons:

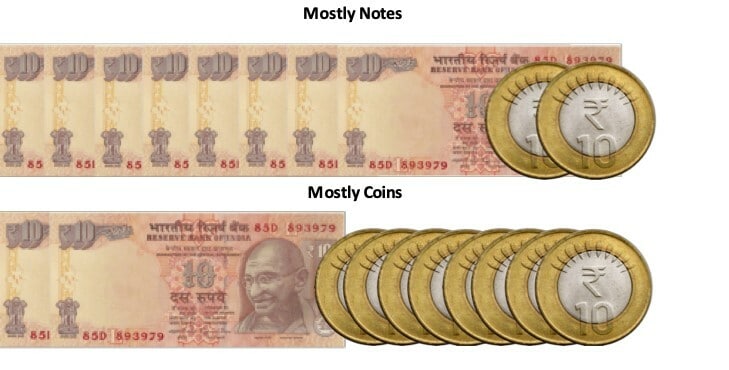

The Indian Rupee features several denominations, with overlaps between coins and banknotes (10-Rupees here). By giving people either coins or banknotes of 10 Rupees we varied the physical form of the money while keeping the number of coins and notes constant. This allowed us to isolate the impact of the physical form of the cash on spending.

India has been consistently one of the most cash-reliant countries in the world. If we found that these practiced cash-users spent more coins than notes, we would cast doubt on the possibility that increased spending of coins is due to a lack of familiarity with the cash.

The rural, Indian setting allowed us to access poorer people, earning as little as 400 Rupees (about 5 Euro) a day. This gave us insight into how they spend their cash. We could endow these people with a substantial sum, equivalent to 25% of their daily income. If even very poor people spend more coins than banknotes, this behaviour might be very common.

We stopped prospective shoppers just outside of a rural shop, offering them 100 Rupees if they answered a few survey questions about the shop. Some shoppers completed the survey with our help because they were illiterate. Shoppers were then paid their money in either mostly 10-Rupee coins or mostly 10-Rupee banknotes.

Outside the shop

Inside the shop, another research assistant, pretending to be a shop assistant, would fetch the goods from the shelves. The shelves were stocked with a variety of both necessities and non-necessities, such as grains, chocolates, and soap. Shoppers would pay at the cash register operated by the shopkeeper.

Cash provided

Firstly, our shoppers clearly preferred spending their coins before their banknotes (irrespective of the number of coins or banknotes they received). Secondly, this translated to a higher overall spending amount for those shoppers who received primarily coins (153 Rupees) than for those who received primarily banknotes (112 Rupees). For a full discussion of these results, please see the technical report.

Finding 2: The Pain of Holding

While our Indian study showed that people spend more when they have coins, it doesn’t explain why. Indeed, the effect we found could be due to something particular about Indian shoppers, or the act of shopping at a store. We therefore followed up our experiment with European and American consumers, and instead of shopping at a store we asked people how much they would donate to a beggar.

In two online experiments in early 2019 we asked Americans and then Europeans to imagine visiting Hong Kong. We asked them to imagine receiving 100 Hong Kong Dollars in change (about 11 Euros) from a taxi driver. This change was either given to them in 10 coins or 10 banknotes. Participants then told us to what extent this money would be a pain (nuisance, annoyance, bother, irritation) to hold on to. Finally, they were asked to imagine walking past a beggar. How much would they donate?

Not only did Americans and Europeans expect that the coins would be more of a pain to hold on to than the banknotes, but this pain of holding also led to a greater intention to donate to the beggar: overall, people with coins intended to give 26% more. Further details of both experiments are provided in the technical report.

Digital Money to Help People Save

Knowing that many people, both rich and poor, spend more coins than banknotes simply because they are more of a pain to hold on to, we turned to trying to help them save this money. Digital money such as credit cards are usually considered less of a pain to pay with, and therefore worse for saving money. However, we expected that giving people the opportunity to ‘digitalize’ their money (i.e., by depositing it into their bank account) might cause them to reconsider spending their coins.

To test if coins might also inspire people to gamble more, we changed the decision to how many lottery tickets people would buy. We tested this in July 2019 in an experiment with European participants, who again imagined receiving 100 Hong Kong Dollars in either coins or banknotes. We asked them how many tickets they might buy in a lottery. We found that participants with coins intended to buy more tickets than those with banknotes, spending 22% more. Furthermore, half of these people were also told that they could easily deposit their coins or banknotes back onto their bank card.

We hoped that those participants who were aware that depositing their coins onto their bank card was an option – and an easy option, too – would choose to spend less of their money on lottery tickets. However, this method proved quite ineffective: participants bought just as many lottery tickets.

Managerial Implications

Despite the proliferation of new forms of payment, cash remains widely in use in both developed and developing countries. At the same time, savings rates across the world are down. We provide evidence that people from both poorer and more developed countries spend more when they have coins than when they have equivalently valued banknotes.

Furthermore, we provide evidence that people spend more because holding on to coins is more of a pain than to notes, which suggests that people spend more than they otherwise would. This spending therefore appears inherently frivolous, and we are now seeking ways in which people can be helped to save more of their coins. We hope that an effective intervention may help to improve the long-term financial well-being of many people around the world.

A Potential Solution

It’s worth trying to limit the number of coins in circulation. After all, if you don’t have coins to spend, you won’t spend them. This could be achieved by phasing out coins altogether – as South Korea has begun to do. Another solution might be a job for retailers: they could leverage existing infrastructure for digital payments (such as through debit cards) to return change not in coins but digitally, straight into their customer’s bank account.

What about countries where such digital infrastructure does not exist, like many developing countries? In those areas, the pain of holding and its potential effect on spending could be taught as part of financial education programs. If individuals become aware that coins make people spend more, they might decide to consciously keep their coins and save them, rather than spend them all too happily.

To read the full report click here.